Key Numbers (Out-of-Sample)

Metrics reported are gross of trading frictions and used primarily for diagnostic comparison, not as live performance claims.

Executive Summary

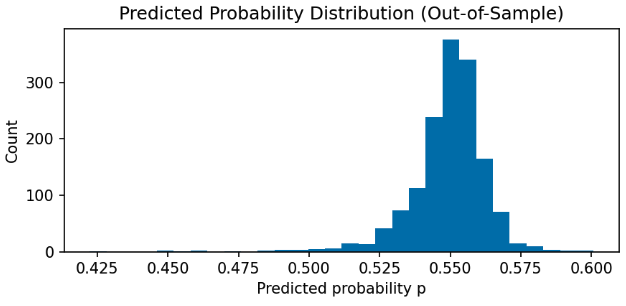

- Daily equity direction prediction is noisy, and predicted probabilities are compressed near 0.5.

- Regimes inferred from returns + realized volatility form persistent market states, not random "clusters."

- Model reliability varies materially by regime, so "average" metrics hide failure modes.

- Filtering trades by confidence and disabling execution in a high-risk regime improves the strategy's risk profile.

What This Demonstrates

- Model risk is conditional: a "single" classifier behaves differently depending on the state distribution it operates under.

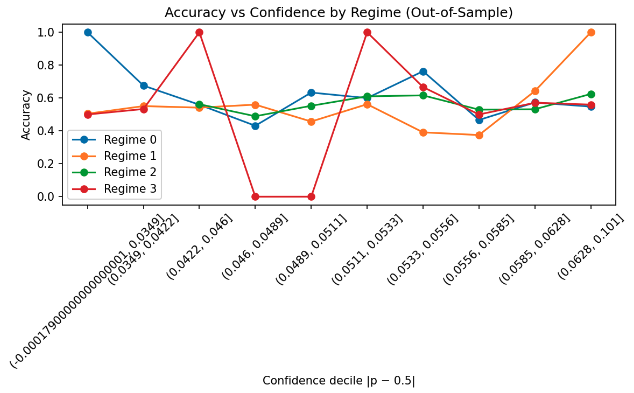

- Confidence is not enough: the confidence-accuracy relationship changes by regime, especially in high volatility.

- Prediction ≠ deployment: economic outcomes are strongly influenced by when you choose to trade, not just what the model predicts.

Methods (Pipeline)

Data

SPY daily closes (2006–2025). Chronological split: 70% train, 30% test.

Features

ret5, vol10, vol20 (standardized on train).

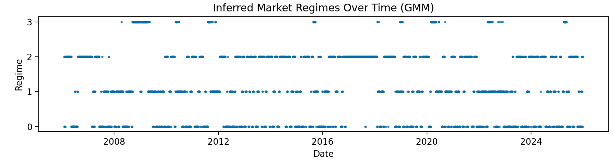

Regimes (Unsupervised)

GMM on (ret5, vol10, vol20) fit on train, then applied forward.

Prediction (Supervised)

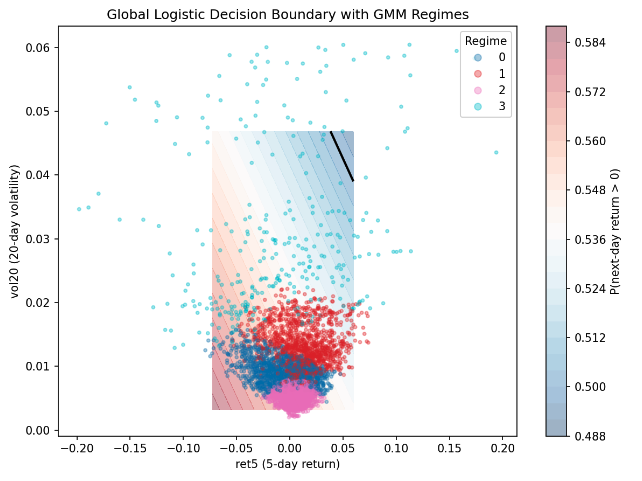

Logistic regression predicts next-day direction using (ret5, vol20).

Confidence

Use |p − 0.5| to stratify reliability and filter trades.

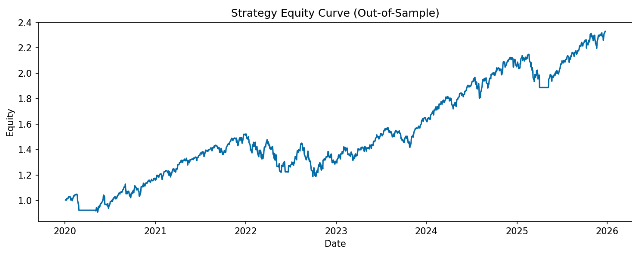

Deployment Rule

Trade only if |p−0.5| > 0.02 and deactivate execution in the high-risk regime.

Evaluation

OOS accuracy by confidence/regime + strategy Sharpe & max drawdown (gross of costs).

Results

Findings

- Regimes persist and cluster in stress periods. The inferred high-volatility state concentrates around extended market stress, consistent with volatility clustering.

- Reliability is regime-dependent. Accuracy patterns differ by regime; the high-volatility regime shows more erratic confidence-stratified behavior (small samples amplify variability).

- Feature-space separation explains it. Regimes occupy distinct regions in (ret5, vol20), so a single global decision rule effectively faces different operating conditions.

- Probabilities are compressed. Outputs stay near the unconditional mean; probabilities work better as low-amplitude signals than as literal calibrated forecasts.

- Deployment rules change the risk profile. Confidence filtering plus deactivating the high-risk regime primarily reduces drawdown depth and return volatility rather than magically increasing raw accuracy.

Regime-Level Strategy Sharpe (OOS)

| Regime | Sharpe | Interpretation |

|---|---|---|

| 0 | 1.38 | Strongest contribution in this regime. |

| 1 | 0.41 | Positive but modest. |

| 2 | 0.22 | Low but positive. |

| 3 | NaN | Unstable / adverse high-volatility state. |

Confidence filter: trade only when |p−0.5| > 0.02, and deactivate execution during the high-risk regime.

High-vol regime clusters around prolonged stress episodes, supporting interpretation as persistent market states.

Confidence is not universally monotonic. High-vol regime shows degraded stability (and smaller bin counts).

Selective deployment changes drawdowns/volatility more than it changes raw predictive metrics. Gross of costs.

Regimes occupy distinct areas of (ret5, vol20), providing a geometric explanation for state-dependent behavior.

Predicted probabilities concentrate near the unconditional mean, motivating thresholded deployment.

Interpretation & Limitations

- Diagnostic, not "alpha claims." The point is to map failure modes and decide when not to trade.

- Costs not modeled. Results are gross of transaction costs, slippage, and financing/short constraints.

- Small samples in extreme regimes. High-volatility regime bins can be thin; interpret bin-level spikes cautiously.

- Next steps. Richer features, alternative regime definitions, and explicit execution costs would make the deployment test more realistic.